AHTS valuation Malaysia engagements sit at the centre of the Malaysian offshore vessel market. The fleet is anchored in Labuan IBFC ownership structures, mobilised from Kemaman as the primary East Malaysia and Sabah staging port, and chartered overwhelmingly into Petronas-driven activity in the Malaysian, Vietnamese, Indonesian, and Bruneian offshore basins. The valuation work that supports this fleet covers marine mortgages, MFRS impairment, charter-back deals, distressed sales, and fleet M&A. The methodology choices, market context, and operational details are specific enough that a generic vessel valuation framing leaves material gaps.

This article sets out the fleet context, the technical definitions that distinguish AHTS from PSV from OSV, the value drivers that move pricing on each vessel class, the methodology choices the valuer makes, the cycle context that any current valuation must reflect, and the workflow MacReal applies to AHTS and supply vessel engagements out of Labuan and Kemaman.

The audience is offshore shipowners managing fleet operations and capital structure, charterers running tonnage requirements, banks underwriting marine mortgages on offshore tonnage, marine insurers calculating sums insured on high-value units, and lawyers handling offshore charter disputes, mortgage default, and fleet M&A.

The Malaysian Offshore O&G Fleet Context

The Malaysian offshore vessel market is structurally driven by Petronas. Petronas Carigali, Petronas operating partners (Shell, ExxonMobil, Hess, Repsol, PTTEP, JX Nippon, and Petronas-led PSCs), and the Petronas LNG and downstream operations together generate the bulk of demand for AHTS, PSV, and OSV tonnage in Malaysian waters. Charter activity is concentrated around platform supply runs, anchor handling for jack-up rig moves, towage of barges and accommodation units, ROV support work, and standby and rescue duties.

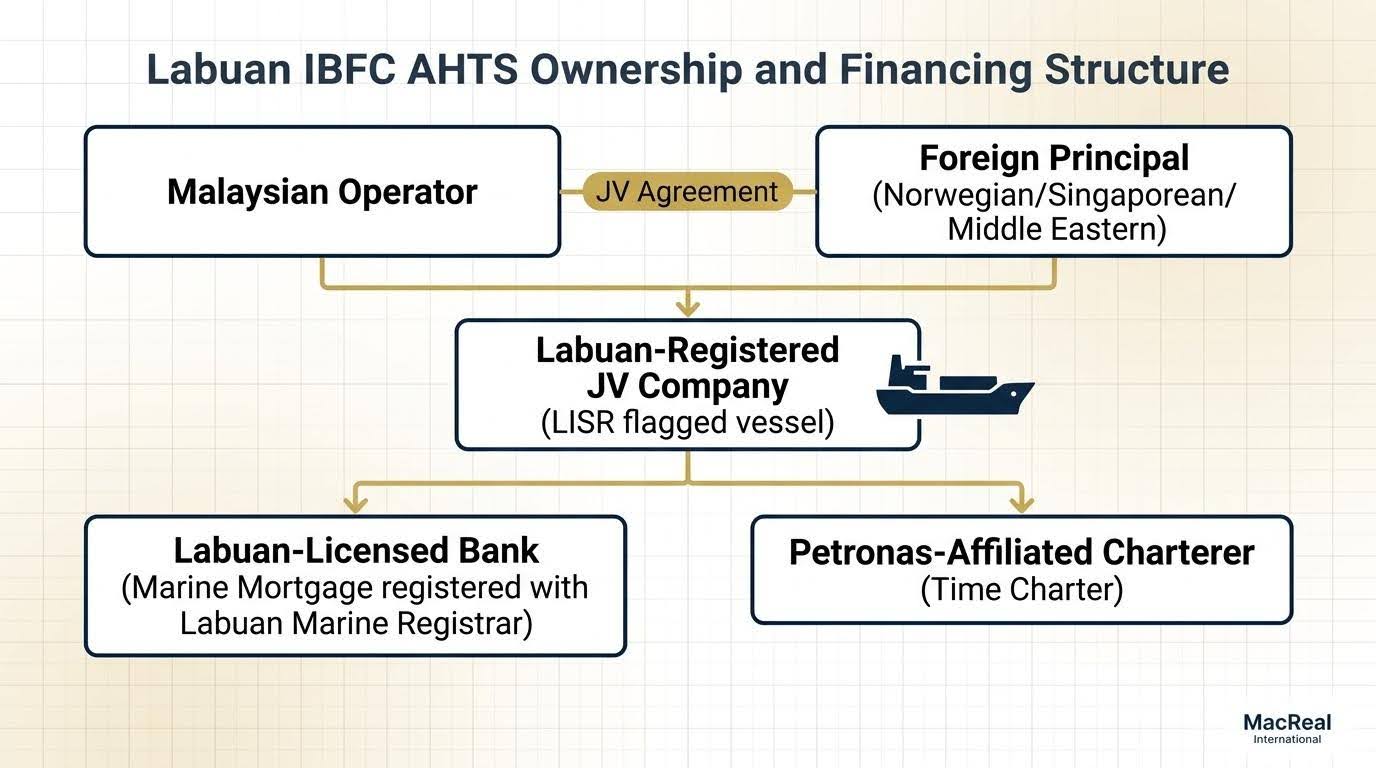

Labuan IBFC as the Ownership Centre

Labuan IBFC is the dominant ownership location for Malaysian-controlled offshore tonnage. The Labuan International Ship Registry (LISR) hosts most of the country’s commercial offshore fleet, and ownership commonly sits in Labuan-licensed companies with structured tax positions, often in joint ventures with Norwegian, Singaporean, Indian, or Middle Eastern principals. The marine mortgage typically sits with a Labuan-licensed bank or with a Malaysian bank operating through its Labuan branch.

The Labuan IBFC Authority and the Labuan Marine Registrar between them publish guidance on registry, mortgage, and operating requirements that any valuation report must reflect.

Kemaman as the East Coast Peninsular and Sabah Staging Port

Kemaman Supply Base in Terengganu is the primary East Coast Peninsular Malaysia staging port for offshore activity in the Peninsular Malaysia basin and the southern South China Sea. AHTS, PSV, and OSV units mobilise from Kemaman to platform clusters off Kerteh, Tapis, and Pulai. Bintulu and Lumut also serve offshore activity, with Bintulu covering the Sarawak basin and Lumut serving the West Coast and Andaman Sea.

For Sabah-based activity, Labuan itself functions as the staging port, supplemented by Kota Kinabalu. The choice of staging port matters for valuation only at the inspection step, where the valuer must travel to the vessel’s port of attendance.

AHTS vs PSV vs OSV: Definitions and Capability Classifications

The three vessel classes are often grouped colloquially as “offshore support vessels” but they value differently and the report should classify the vessel precisely.

AHTS (Anchor Handling Tug Supply)

AHTS units combine anchor handling capability for jack-up rig and semi-submersible moves with platform supply duties and towage. Key capability descriptors include:

- Brake Horse Power (BHP), typically ranging from 4,000 BHP for small AHTS to over 24,000 BHP for deepwater AHTS

- Bollard Pull (BP), typically 60 to 250 tonnes

- Deck space and deck strength for cargo and pipe handling

- Fuel oil, fresh water, drill water, and brine capacity

- Dry bulk capacity (cement, barite, bentonite)

- Accommodation berth count

- Dynamic Positioning class (DP1, DP2, DP3) where applicable

- Winch capacity for anchor handling

A typical Malaysian working AHTS sits in the 5,000 to 12,000 BHP and 80 to 180 BP range, with DP2 capability increasingly common for newer units.

PSV (Platform Supply Vessel)

PSV units focus on platform resupply duties: fuel, water, dry bulks, deck cargo, and personnel transfer. They have larger deck space and bulk capacity than AHTS units of equivalent length, but lower bollard pull and no significant anchor handling capability. DP class is standard on modern PSV units.

OSV (Offshore Support Vessel) as the Generic Category

“OSV” is a broad category that includes AHTS, PSV, and other support vessel types such as accommodation, ROV support, dive support, well intervention, and crew boats. When a charter party or registry document refers to an OSV, the valuer should classify the vessel into the specific sub-type.

Key Value Drivers for AHTS and Supply Vessels

Five drivers do most of the work in moving the value of an AHTS or supply vessel.

Charter status and tenor. A vessel on a long-tenor Petronas charter values materially differently from a vessel on the spot market or laid up. The charter rate, charter tenor, charter renewal probability, and counterparty credit standing all flow into the valuation. A long-tenor Petronas charter at above-market rates lifts the vessel value through the income approach.

Classification status. The classification society of record (Lloyd’s Register, ABS, DNV, Bureau Veritas, Indian Register of Shipping, Nippon Kaiji Kyokai), the current class notation, the next due dates for special survey and intermediate survey, and any outstanding conditions of class are all material. Suspended or withdrawn class drops the value sharply because the vessel cannot trade or be financed by reputable lenders.

BHP, BP, deck specs, and DP class. Higher BHP and BP, larger deck space, higher bulk capacity, and DP2 or DP3 class all command value premiums. The premium is largest where the vessel’s capability matches the demand profile of the active charter market in Malaysia and the wider Southeast Asia region.

Age and refurbishment history. AHTS and supply vessels follow age depreciation curves that flatten significantly after major refurbishment programmes. A 15-year-old AHTS with a recent comprehensive refurbishment values closer to a 10-year-old benchmark than to a chronological 15-year benchmark.

Market cycle position. Offshore vessel values are heavily cycle-driven. The post-2014 oil price reset, the 2020 demand collapse during the pandemic, and the post-2022 demand recovery all moved values by 30 to 60 percent across the cycle. Any current valuation must explicitly identify where the market sits in the cycle and reflect the cycle context in the value conclusion.

Indicative cycle context for AHTS and PSV asset values from the post-2014 oil price reset through the 2020 demand collapse and the post-2022 recovery.

Valuation Methodology for AHTS and Supply Vessels

The methodology choice depends on the vessel’s charter status and the depth of the comparables base.

Market Approach for the Active S&P Market

Where the market for the relevant vessel size and capability is active, with recent sale and purchase (S&P) comparables, the market approach is the default. The valuer sources comparables from Clarksons Research, VesselsValue, BIMCO market reports, and direct broker contacts in Singapore and the regional offshore brokerage market. The valuer adjusts comparables for vessel age, BHP, BP, DP class, charter status, and yard pedigree.

Income Approach for Time-Charter Committed Vessels

Where the vessel is on a long-tenor time charter, particularly to a Petronas-affiliated charterer with strong counterparty credit, the income approach is appropriate. The valuer models the charter cash flow over the remaining tenor, applies an appropriate discount rate reflecting the asset risk, the counterparty credit, and the residual value risk, and reaches a value conclusion that reflects the charter premium or discount.

The discount rate selection is the most sensitive input. For a Petronas-chartered Labuan-flagged AHTS, a discount rate in the high single digits to low double digits (in MYR) is typical, depending on tenor, counterparty, and residual assumptions.

Depreciated Replacement Cost (DRC) for Unique High-Spec Assets

DRC applies where the vessel is sufficiently unique that the comparables base is thin. Examples include high-spec deepwater AHTS units with DP3, very high BHP, and specialised equipment fits. The valuer estimates current new-build replacement cost in a relevant yard, applies physical depreciation against effective age, and adjusts for functional and economic obsolescence.

Combined Approach in Practice

Most Malaysian AHTS and supply vessel reports combine market and income approaches, with the market approach providing the charter-free anchor and the income approach providing the charter premium or discount. Where comparables are thin, DRC is used as a secondary cross-check.

Cycle Context: Post-2014 Reset and Post-2020 Recovery

A defensible AHTS or supply vessel valuation cannot ignore the cycle context.

Post-2014 reset. The oil price collapse from late 2014 through 2016 cut offshore E&P spending sharply. Day rates and asset values fell 40 to 60 percent across most AHTS and PSV classes. A wave of newbuilds delivered into a contracting market, lengthening the trough.

2018 to 2019 partial recovery. Day rates recovered modestly as supply attrition (scrapping, lay-up, conversion) tightened the active fleet, but values remained well below the pre-2014 peak.

2020 demand collapse. The pandemic triggered a sharp demand drop that pushed many units into cold lay-up.

Post-2022 demand recovery. The combination of oil price recovery, energy security drivers, and offshore E&P spending recovery has tightened the AHTS and PSV market through 2023 to 2026. Day rates and asset values have recovered substantially, particularly for higher-spec DP2 and DP3 units. The recovery is uneven by vessel type, age, and region.

The Malaysian fleet has tracked the global cycle but with regional nuances driven by Petronas activity. Any valuation as of 2026 should explicitly reference the cycle position, source the day-rate environment from current Clarksons Research or equivalent data, and reflect the relevant supply-demand balance.

Labuan IBFC Marine Financing Structures

The Labuan IBFC framework supports several common financing structures for AHTS and supply vessel acquisitions.

Labuan Marine Charter (LMC) structures. Some operators hold tonnage through Labuan structures designed to optimise charter and ownership tax treatment. The valuation report must reflect the charter chain accurately.

Joint ventures with foreign principals. Norwegian, Singaporean, Indian, and Middle Eastern principals frequently partner with Malaysian operators through Labuan JV structures. The JV structure can affect the ownership chain in the registry and the security package in the marine mortgage. The valuation report should disclose the JV structure where material.

Labuan-licensed bank financing. The marine mortgage typically sits with a Labuan-licensed bank or a Malaysian bank operating through its Labuan branch. The credit committee is most often based in Kuala Lumpur or Singapore.

Petronas-driven charter assignments. Where the charter is to a Petronas-affiliated charterer, the bank often takes assignment of charter receivables as part of the security package. The valuation report should reflect the charter party terms relevant to the assignment.

Common Use Cases for AHTS and Supply Vessel Valuations

Malaysian AHTS and supply vessel valuations span six recurring use cases.

Marine mortgage. Initial drawdown valuations and annual or biennial revaluations for facilities with Labuan-licensed and Malaysian banks. See the companion article on vessel valuation for marine mortgage and bank financing for the bank-side workflow.

MFRS impairment. Listed and audited Malaysian shipowners require MFRS 36 impairment reviews on vessel cash-generating units. The valuation supports the recoverable amount calculation, drawing on either fair value less costs of disposal or value in use.

Charter-back deals. Where a shipowner sells a vessel and immediately charters it back, the sale price and charter rate must be supported by an independent valuation to demonstrate fair value to auditors and regulators.

Distressed sale. Where a borrower defaults or restructures, a forced sale value (FSV) report supports the lender’s recovery position and the borrower’s commercial discussions.

Fleet M&A. Acquirers of shipping companies need fleet-level valuation work that combines per-vessel valuations with fleet-level operating economics. See vessel valuation in Malaysia M&A and fleet acquisition and business valuation for M&A in Malaysia for the M&A overlay.

Insurance reinstatement. Marine insurers and brokers commission valuations to set sums insured, validate reinstatement claims, or arbitrate total loss settlements.

Typical Labuan-registered AHTS held through a JV between a Malaysian operator and a foreign principal, on charter to a Petronas-affiliated charterer.

The MacReal Process for AHTS Engagements

MacReal’s AHTS and supply vessel engagements follow a defined workflow that reflects the operational realities of the Malaysian offshore market.

Step one: scoping call. Capture vessel particulars (name, IMO number, year built, builder, BHP, BP, DP class, classification society, current charter, current location), the use case, the deliverable required, and the timeline. For Labuan-registered units, identify the registry, the mortgage holder, and the JV structure if any.

Step two: document checklist. Comprehensive document request covering certificates of registry, classification certificates and survey records, drydocking history, charter party documents, recent surveyor reports, ownership chain documents, JV agreements where material, insurance documents, and any prior valuation reports.

Step three: market research and comparables. Source comparables from Clarksons Research, VesselsValue, BIMCO market reports, and regional broker contacts. Cross-check against any recent S&P transactions in the Malaysian and Singapore markets and any data published by the Malaysia Shipowners’ Association (MASA).</span>

<b>Step four: inspection. On-board attendance at the vessel’s port (Labuan, Kemaman, Bintulu, Lumut, or Port Klang depending on the vessel’s location). Structured condition walk-through with photographic record of hull, machinery space, deck equipment, anchor handling and towing equipment, navigation and DP electronics, accommodation, and lifesaving and firefighting equipment.</p>

Step five: methodology and analysis. Apply market approach as primary, income approach where charter status warrants, DRC wh

ere comparables are thin. Reconcile the three approaches into a single value conclusion with full disclosure of methodology, inputs, and reasoning.</p>

<b>Step six: report and review. Draft delivered for client and (where applicable) bank review. Final signed report issued wi</span>

th all required value definitions (MV charter-free, MV charter-attached, FSV charter-free where bank requires).

Step seven: post-issuance support.</b><span style=”font-weight: 400;”> MacReal can attend bank credit committee, audit committee, or court hearings to discuss the report, methodology, and value conclusion.

Related Reading

For broader context, see MacReal’s pillar guide on vessel valuation in Malaysia, the companion article on OSV valuation, and the Malaysia shipping industry market overview. For Labuan-specific structuring, see Labuan IBFC shipping vessel valuation considerations. For methodology depth on classification, see classification society status and vessel value. For the bank-side process, see vessel valuation for marine mortgage and bank financing. For the M&A overlay on fleet transactions, see business valuation for M&A in Malaysia.

Get an AHTS or Supply Vessel Valuation

If you have an AHTS, PSV, or OSV in Labuan IBFC, Kemaman, Port Klang, Bintulu, or Lumut that needs valuation for marine mortgage, MFRS impairment, charter-back, distressed sale, or fleet M&A, contact MacReal International. The intake call takes 30 minutes for offshore engagements and the written quote lands within one business day.